|

|

|

|

An Analysis of Financial Practices in Client Dispute Resolution

Sarah Shaikh 1![]() ,

Dr. Bhojraj Shewale 2, Bhawna

Sharma 3

,

Dr. Bhojraj Shewale 2, Bhawna

Sharma 3

1 BBA

3rd Year (Hons), Amity Business School, Amity University, Mumbai, India

2 Assistant

Professor, Amity Business School, Amity University, Mumbai, India

3 Director International Affairs and Programs, Officiating HOI, Amity

Business School, Amity University, Mumbai, India

|

|

|

ABSTRACT |

|

|

The investigation not only reveals a singular but also multifaceted nature of the relationship between accounting technologies and the financial record management process in a firm that provides audit, taxation, and consultancy services. The adoption of digital accounting systems such as Tally Prime has brought about the complete extinction of manual bookkeeping, thus leading to the migration of firms toward fully automated financial management. Among the software benefits being trials are the reduction of human errors, the speed of data processing, and finally, improved decision-making. The researcher adopted descriptive and mixed-method research approaches, making use of both primary data (obtained through observation and interaction with staff) and secondary data (from accounting manuals and software documentation). The research

reveals that Tally Prime tremendously boosts efficiency, cuts down human

errors to a minimum, and secures compliance with legal standards. However,

the firm continues to experience a number of issues such as inadequate user

training, the need for data synchronization, and system updates. One of the

conclusions drawn from the research is that the use of accounting software is

a key factor in uplifting the professionalism of accountants in terms of

accuracy, speed, and transparency of financial record-keeping. |

|||

|

Received 05 September 2025 Accepted 29 October 2025 Published 24 November 2025 DOI 10.29121/ShodhSamajik.v2.i2.2025.47 Funding: This research

received no specific grant from any funding agency in the public, commercial,

or not-for-profit sectors. Copyright: © 2025 The

Author(s). This work is licensed under a Creative Commons

Attribution 4.0 International License. With the

license CC-BY, authors retain the copyright, allowing anyone to download,

reuse, re-print, modify, distribute, and/or copy their contribution. The work

must be properly attributed to its author.

|

|||

|

Keywords: Financial Management, Client Escalations, Debt

Recovery, Ethical Finance, Documentation Accuracy, CRM Software, Rbi

Compliance, Digital Automation |

|||

1. INTRODUCTION

1.1. Background

Finance is the backbone of every organization, therefore influencing all the departments and the whole decision-making process. The want or ability of the company to have its financial records accurately and consistently maintained is a very strong point that directly relates to its credibility, client relations, and operational success. The financial aspect of service-oriented industries, especially debt management and recovery, is very sensitive since it entails much customer engagement through, for example, discussions on overdue payments, settlements, and even reconciliations.

When a client escalates an issue, this is usually an indication that the problem or disagreement has been referred to a higher authority. Client escalations are often the effect of delay, error, or simply dissatisfaction. If these escalations are not managed properly, then they will result in loss of trust, termination of the contract, damage to the company's reputation, and possibly reputational damage. Hence, knowing how finance plays a part in escalation management is of prime importance as it will tell us a lot about the company's communication, accountability, and ethics practices.

1.2. Context of the Study

This research will be done at the company, a company that has been in the debt management business for over two decades. From the beginning of the year until now, this company partnered with banks and NBFCs to recover overdue payments from customers. The operations are based only on ethical compliance with RBI guidelines and the use of certified DRAs. The firm's processes are representative of how financial discipline supports transparency, client satisfaction, and regulatory adherence-all of which can influence escalation outcomes.

1.3. Rationale

Even small cases of financial mismanagement can create misunderstandings and cause clients to complain more loudly than before. In the modern corporate world, where client relations are more and more data driven, the finance teams need to work very closely with the operational and service departments. The objective of the research is to facilitate the meeting of academic knowledge with corporate application through the demonstration of financial integrity as a contributor to the reduction of conflicts.

1.4. Research Problem

The main issue to be investigated is:

What are the implications of financial management practices on the emergence, escalation, and resolution of customer complaints in a business organization?

1.5. Objectives

Goals of the study include:

· The purpose is to analyze the position finance holds in escalation management.

· The insight into how documentation and accuracy influence client relations should be gained.

· To analyze the financial structure and the escalation process of the business.

· To spot difficulties and propose practical renovations.

· To explore the relationship between ethical finance and sustainable corporate reputation.

2. Literature Review

2.1. Finance and Client Relations

According to the Reserve Bank of India. (2024), the foundation of durable client relationships consists of transparency and reliability in terms of financial aspects. Financial errors or miscommunication are the most frequent causes of client complaints. A study by Financial Express. (2023)stated that over 60% of escalations for clients in the BFSI sector result either from disputes over bills or from delayed payments.

2.2. Escalation Management in Corporate Settings

Escalation management is the structured resolution of client complaints referred to higher management for quick resolution. Kumar and Sinha (2022) indicated that the resolution of an escalation depends on effective documentation, inter-departmental collaboration, and access to data. Finance is, therefore, a pivotal point in this system because the majority of client conflicts pertain to the movement of money, the accuracy of payments, or the reconciliation of accounts.

2.3. Ethics and Financial Compliance

Ethical governance is essential for financial operations management. The Indian Banks' Association (2022) recommends that strict adherence to the code of conduct of recovery agents as prescribed by the RBI be followed. Ethical practices are useful in the finance industry as they reduce conflict, and strengthens brand identity, and this is perceived positively especially in sectors prone to reputational damage, such as debt management.

2.4. Making Technology and Financial Decisions

After researching, it has been identified that automation and artificial intelligence (AI) analytics are changing the way finance is managed. Based on the information from The Economic Times. (2023), it seems the trend is to improve financial transparency and the efficiencies of tracking systems through using automated systems for accurate financial reporting and management. In customer-facing operations, the technology helps to overcome human error and prevents mistakes from happening.

3. Theoretical Framework

This research is aligned with two key management theories:

3.1. Financial Control Theory

Financial Control Theory postulates that effective financial monitoring and data management provide grounds for better organizational decision-making. Based on this theory, the possibility of client escalations could be at minimal since firms would exert due control over their respective financial processes in a manner that ensures transparency and accountability.

Parasuraman et al. (1988) SERVQUAL model considers five dimensions of service quality: reliability, responsiveness, assurance, empathy, and tangibility. In the context of debt management, financial transparency and communication directly impact these dimensions, which in turn affect client satisfaction and escalation rates.

These theories together show that consistent financial control, coupled with quality-focused service, advances the stability of organizations by reducing conflicts. Increasing competition due to technology-driven startups.

4. Research Methodology

4.1. Research Design

This study adopts a qualitative and descriptive research design. The data were gathered during the six-week internship period in the company, which gave practical exposure to financial documentation, communication with clients, and escalation processes.

The CRM software lets multiple departments to view the status of a case in real time. This lowers miscommunication, speeds up transactions, and creates accountability.

4.2. Data Collection

Primary Data: Observations of daily operations, informal interviews with employees, and analysis of CRM (Customer Relationship Management) entries.

Secondary Data: RBI guidelines and policies, company manuals, financial reports, and academic papers on debt recovery practices.

4.3. Data Analysis

A thematic analysis method identified patterns in financial decision-making, client communication, and escalation outcomes. Each observation was categorized under documentation accuracy, communication flow, and financial compliance.

4.4. Scope and Limitations

Since the research is performed in only one organization and a certain period of internship, generalization may not be possible. However, it can provide insights valuable to similar firms operating in the BFSI sector.

4.5. Understandings

The organisation benefits from a strong foundation built over two decades, with a well-established reputation and certified recovery professionals who operate with transparency and ethical standards. Its long-standing partnerships with major financial institutions further reinforce trust and credibility in the market.

However, there are areas that present internal challenges. The organisation has not yet fully embraced advanced digital tools, which limits efficiency and scalability. Employees often experience stress due to the demanding nature of fieldwork, and the business relies heavily on a few major clients, which can create vulnerability. Additionally, the brand’s presence outside of its core B2B segment remains modest.

At the same time, the external environment presents notable opportunities. The increasing adoption of digital automation and AI can significantly improve predictive recovery and streamline processes. Collaborations with fintech firms can open avenues for innovation, while expansion into credit counselling and analytics services offers potential for diversification and growth.

There are also external risks to consider. Regulatory frameworks are becoming stricter, especially with evolving RBI guidelines, which may require operational adjustments. Public perception of recovery agencies can be a challenge, as negative views may impact reputation and client interactions. Moreover, technology-driven startups are intensifying competition, pushing traditional firms to evolve rapidly to remain relevant.

5. Industry Analysis

5.1. Overview

This industry is part of the broad BFSI sector in India. Debt management plays a very important role in financial sustainability by helping institutions recover funds that otherwise would have been lost to defaults.

5.2. Market Dynamics

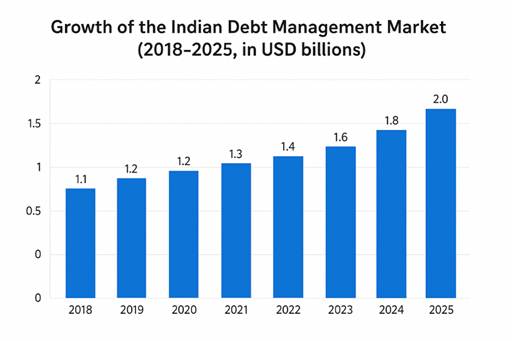

The debt management market of India is approximately USD 1.5 billion in value for the year 2025, growing at an annual rate of 7–8% per annum, driven by:

Expansion of retail credit and digital lending.

Government initiatives promoting financial inclusion.

5.3. Significant Factors

1) Adherence to Regulatory Standards: RBI has stipulated that recovery must be engaged through appropriate channels.

2) Technology Integration: Innovations of AI and automation are increasing the efficiency of processes.

3) Financial Awareness: Customers like repayment structures that are transparent.

5.4. Challenges

· Despite the growth, the industry also faces:

· Public stigma towards recovery agencies.

· Employee burnout due to demanding targets.

· Delayed client payments that impact agency cash flows.

5.5. the business's Position

the business stands out for its compliance, training infrastructure, and client relationships. Its transparent financial operations and skilled workforce enable it to maintain a competitive edge in a reputation-sensitive industry.

6. Findings and Discussion

The internship revealed several findings linked to finance and the dynamics of client escalation:

6.1. Financial Records Prevent Escalations

Accurate record-keeping ensures clear communication with clients. At the business, every financial transaction—from invoices to credit notes—is verified before submission, reducing disputes.

6.2. CRM Improves Transparency

The CRM software enables departments to simultaneously monitor case advancement. This reduces the potential of misunderstanding, becomes more efficient in decision-making, and creates accountability.

6.3. Finance and Risk Relationship

the enterprise follows the RBI Code of Conduct. All actions taken related to recovery are done compassionately/humanely and with respect for clients. Ethics will serve as the cornerstone for engagement at the enterprise so as to ensure long-term relationships and a positive brand image.

6.4. Ethical Finance Creates Client Trust

The Code of Conduct for RBI is strictly adhered to by the business and all activities taken for recovery, starting from the assignment, are to be humane and respectful. Structuring people, processes and systems on the premise of ethics strengthens long-term relationships and preserves brand image.

6.5. Working Across Departments

Managing escalations is a collaborative process between departments (finance/operations/client service).

This cooperation ensures that financial errors are quickly corrected and that client concerns are effectively addressed. Escalation management requires the team members from finance, operations, and client services departments to work together.

Due to increased competition from new technology driven startups.

· Developing Data Analytics Division: Create a dedicated analytics team to present the repayment trends and give insights to clients in real time for effective decision-making.

· Diversification of Service Portfolio: Expand services to early delinquency management, portfolio auditing, and credit counseling.

· Rural Outreach: Engage in partnerships with microfinance institutions and regional banks for the expansion of the client base and to promote financial inclusion.

· Enhancing Employee Welfare: Public Awareness Programs: Hold community programs and campaigns that highlight model ethical recovery practices to help in improving public perceptions.

7. Suggestions

· Digital Modernization: Commit to the implementation of artificial intelligence to track recovery, create automated dashboards, and develop a cloud-based documentation system that is accurate and scalable.

· Enhancing Agent Training: Offer refresher courses that include ethics, communication, and emotional intelligence aimed at developing agent professional ability to cope with stress and stayed professionalism.

· Analytics Division: Allocate resources to enable an analytics team that can develop repayment trends and present them to clients in real-time to incorporate into decision-making.

· Expansion of Services: Expand the services offered for early delinquency management, portfolio auditing and credit counseling.

· Rural Focus: Partner with regional banks and microfinance institutions to increase client base and support financial inclusion.

· Improving Employee Benefits: Increasing or enhancing the additional advantages employees receive to ensure their well-being, satisfaction, and motivation.

8. Conclusion

The study concludes that financial management and escalation control are closely linked in modern organizations. The company demonstrates how disciplined financial operations, ethical compliance, and clear communication can effectively minimize client escalations. Financial accuracy enhances institutional trust and ensures corporate stability and reputation. This internship experience made it clear: finance is not all about numbers; it's also a behavioral and relational function that, when treated in an ethical and strategic manner, can help maintain good relationships between organizations and their clients. As industries go digital, investment in technology, training, and analytics is imperative on the part of the business to maintain its leading position in the industry of debt management. It can set new benchmarks for responsible, ethical, and financially sound corporate practices that promote both business growth and societal well-being.

CONFLICT OF INTERESTS

None.

ACKNOWLEDGMENTS

None.

REFERENCES

Bajaj Finance Ltd. (2023). Debt Recovery

Operations and Compliance Updates. Corporate

Financial Reports.

Financial Express. (2023). Rise in Customer Escalations in the BFSI Sector due to Billing Disputes

and Payment Delays.

Financial Express Reports.

HDFC Bank. (2023). Retail Credit

Performance and Overdue Accounts

Management. HDFC Industry Report.

Indian Banks’ Association. (2022). Code of Conduct for Recovery Agents: Best Practices and Compliance Standards. IBA

Publications.

Kumar, R., & Sinha, A. (2022). Escalation Management and Service Recovery in Corporate organizations. Journal of Business and Service Management,

14(2), 45–58.

Parasuraman, A., Zeithaml, V., & Berry, L. (1988). SERVQUAL: A Multiple-Item Scale for Measuring Consumer

Perceptions of Service Quality. Journal of Retailing, 64(1), 12–40.

Reserve Bank of India. (2024). Guidelines on Recovery agents and Fair

Practices in Loan Recovery. RBI Publications.

Sinha, P. (2023). Ethical Finance Practices and Organizational Transparency in Debt Collection Agencies.

International Journal of Corporate Governance, 11(3), 66–78.

The Economic

Times. (2023). Automation and AI-Driven Financial Reporting Trends in India’s BFSI Sector. Economic Times

Insights.

The enterprise Enterprises. (2024). Company Manuals, Operational Guidelines, and Financial Process Documents.

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© ShodhSamajik 2025. All Rights Reserved.